What Is Life Insurance for Seniors Over 60?

Life insurance for seniors is a policy designed for individuals aged 60 and above. It pays a death benefit to beneficiaries, helping cover expenses like:

- Funeral and burial costs

- Outstanding debts

- Medical bills

- Income replacement for dependents

Unlike policies for younger individuals, senior plans often feature simplified underwriting, smaller coverage amounts, and flexible approval options.

Why Life Insurance Matters After Age 60

At this stage of life, financial priorities shift. The focus is less on wealth building and more on protection and legacy planning.

Key reasons seniors buy life insurance:

- Avoid burdening family with funeral costs

- Provide financial support to a spouse

- Cover unpaid debts or loans

- Leave inheritance for children or grandchildren

Even a modest policy can prevent significant financial stress for loved ones.

Types of Life Insurance for Seniors

Understanding your options is critical before choosing a policy.

1. Term Life Insurance

- Coverage for a fixed period (10–30 years)

- Lower monthly premiums

- No payout if the term expires

Best for: Seniors who want temporary coverage or income replacement.

2. Whole Life Insurance

- Lifetime coverage

- Builds cash value over time

- Higher premiums but guaranteed payout

Best for: Long-term financial planning and estate transfer.

3. Guaranteed Issue Life Insurance

- No medical exam required

- Guaranteed approval

- Lower coverage ($5,000–$25,000)

Best for: Seniors with serious health conditions.

4. Final Expense Insurance

- Designed for funeral and burial costs

- Simple application process

Best for: Covering end-of-life expenses without complexity.

Best Life Insurance Companies for Seniors (2026)

Several providers consistently rank high for senior-friendly policies:

- AARP – Strong no-exam options for seniors

- Mutual of Omaha – Popular for final expense coverage

- New York Life – High coverage and financial strength

- State Farm – Excellent customer service and agent network

Quick Comparison

| Provider | Best For | Policy Type | Medical Exam |

|---|---|---|---|

| AARP | Seniors 60–80 | Term & Whole | No |

| Mutual of Omaha | Final expense | Whole | Optional |

| New York Life | Large policies | Term & Whole | Yes |

| State Farm | Personalized service | Term | Yes |

How Much Does Life Insurance Cost After 60?

Costs increase with age, but affordable options still exist.

Average Monthly Premiums

| Age | Term Life ($100K) | Whole Life ($25K) |

|---|---|---|

| 60 | $80–$150 | $120–$250 |

| 65 | $100–$200 | $150–$300 |

| 70 | $150–$300 | $200–$400 |

| 75+ | $250+ | $300+ |

What Affects Your Premium?

- Age

- Health condition

- Smoking status

- Coverage amount

- Policy type

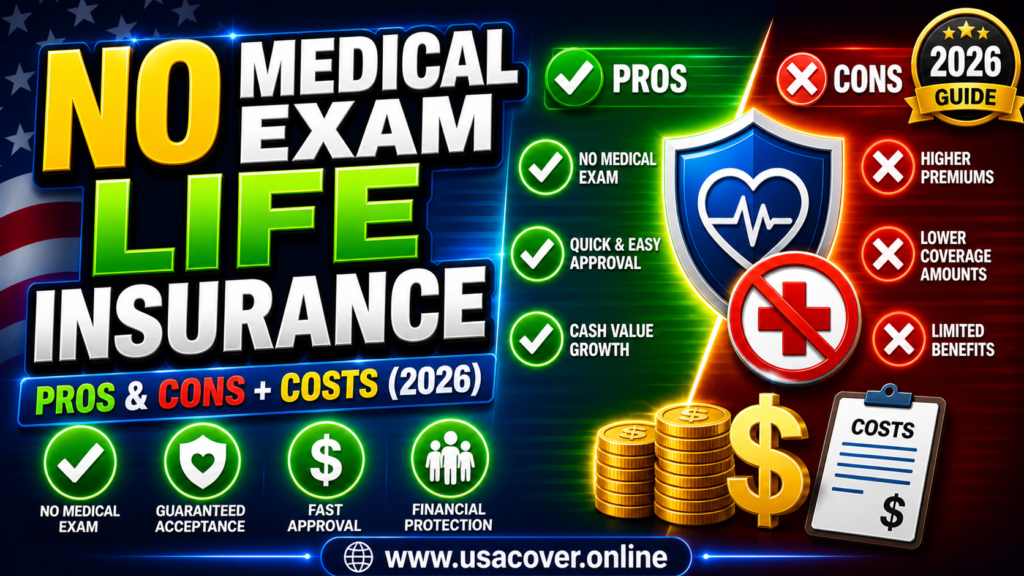

No Medical Exam Life Insurance: Is It Worth It?

No-exam policies are increasingly popular among seniors.

Pros

- Fast approval (sometimes within 24–48 hours)

- No health checkups

- Easy application process

Cons

- Higher premiums

- Lower coverage limits

- Possible waiting periods

Best for: Seniors with health concerns or those needing quick approval.

How to Choose the Best Policy (Step-by-Step Framework)

Step 1: Define Your Goal

- Funeral costs → Final expense insurance

- Income protection → Term life

- Legacy planning → Whole life

Step 2: Evaluate Your Health

- Good health → More affordable options

- Health issues → Consider guaranteed issue

Step 3: Set a Realistic Budget

Avoid overcommitting. Choose premiums you can maintain long-term.

Step 4: Compare Providers

Look at:

- Financial strength

- Customer reviews

- Claim payout reliability

Step 5: Choose Coverage Amount

Typical ranges:

- $5,000–$25,000 → Final expenses

- $50,000–$150,000 → Family support

Real-Life Scenarios

Scenario 1: Healthy 62-Year-Old Retiree

- Chooses term life for $100,000

- Low premium due to good health

Scenario 2: 70-Year-Old with Diabetes

- Opts for guaranteed issue policy

- Accepts higher premium for guaranteed approval

Scenario 3: Couple Planning Legacy

- Purchases whole life policy

- Builds cash value over time

Common Mistakes to Avoid

- Waiting too long (premiums increase with age)

- Choosing cheapest policy without reviewing terms

- Ignoring exclusions and waiting periods

- Not updating beneficiaries

- Buying more coverage than needed

Alternatives to Life Insurance

If traditional life insurance isn’t suitable, consider:

- Savings accounts

- Fixed deposits

- Pension funds

- Annuity

- Employer-sponsored benefits

These options may provide partial financial protection but lack the guaranteed payout of insurance.

Best Practices for Seniors Buying Life Insurance

- Apply as early as possible

- Compare multiple quotes before deciding

- Review policy every few years

- Consider inflation when choosing coverage

- Work with a licensed advisor if needed

Frequently Asked Questions

1. What is the best life insurance for seniors over 60?

Whole life and guaranteed issue policies are often best because they provide lifetime coverage and easier approval.

2. Can a 65-year-old get life insurance?

Yes, many insurers offer policies up to age 80 or even beyond, though premiums will be higher.

3. Is life insurance worth it after 60?

Yes, especially for covering final expenses, protecting dependents, and leaving a financial legacy.

4. What is the cheapest life insurance for seniors?

Term life insurance is typically the most affordable option for healthy individuals.

5. Do seniors need a medical exam?

Not always. Many providers offer no-exam or simplified issue policies.

6. How much coverage should a senior have?

Most seniors choose between $5,000 and $100,000 depending on their financial goals.

7. What happens if I outlive my term policy?

Coverage ends with no payout unless you renew or convert the policy.

8. Which company is best for seniors?

Companies like AARP and Mutual of Omaha are popular due to senior-focused plans.

Conclusion

Finding the best life insurance for seniors over 60 comes down to matching your needs with the right policy type.

If you want affordability, term life may be ideal. If you need lifelong protection, whole life or guaranteed issue policies are better choices.

The key is to act early, compare options carefully, and choose a policy that provides lasting financial security for your loved ones.