What Is No Medical Exam Life Insurance?

No medical exam life insurance is a type of policy that lets you get coverage without undergoing a physical exam. Instead of blood tests or doctor visits, insurers evaluate your risk using:

- Health questionnaires

- Prescription drug history

- Third-party databases like the Medical Information Bureau

- Driving records

This allows approval decisions to happen much faster—sometimes within minutes.

Why It Matters

For many Americans, traditional life insurance can feel slow, invasive, or even inaccessible—especially if you have health conditions.

No exam policies remove that barrier, making coverage faster, simpler, and more accessible, but not without trade-offs.

How No Medical Exam Life Insurance Works

Step-by-Step Process

- Application Submission

Fill out a short online form with personal and health details. - Data Verification

Insurers cross-check your information using databases and records. - Automated Underwriting

Algorithms assess your risk profile using predictive models. - Approval Decision

- Instant approval (in some cases)

- Or within 24–72 hours

- Policy Activation

Coverage begins once you accept and pay the premium.

Types of No Medical Exam Life Insurance

1. Simplified Issue Life Insurance

- Requires basic health questions

- Faster approval

- Moderate coverage limits

2. Guaranteed Issue Life Insurance

- No health questions at all

- Guaranteed approval

- Typically includes a 2–3 year waiting period

3. Accelerated Underwriting Policies

- Uses advanced data and AI

- Offered by companies like John Hancock

- Combines speed with more accurate risk assessment

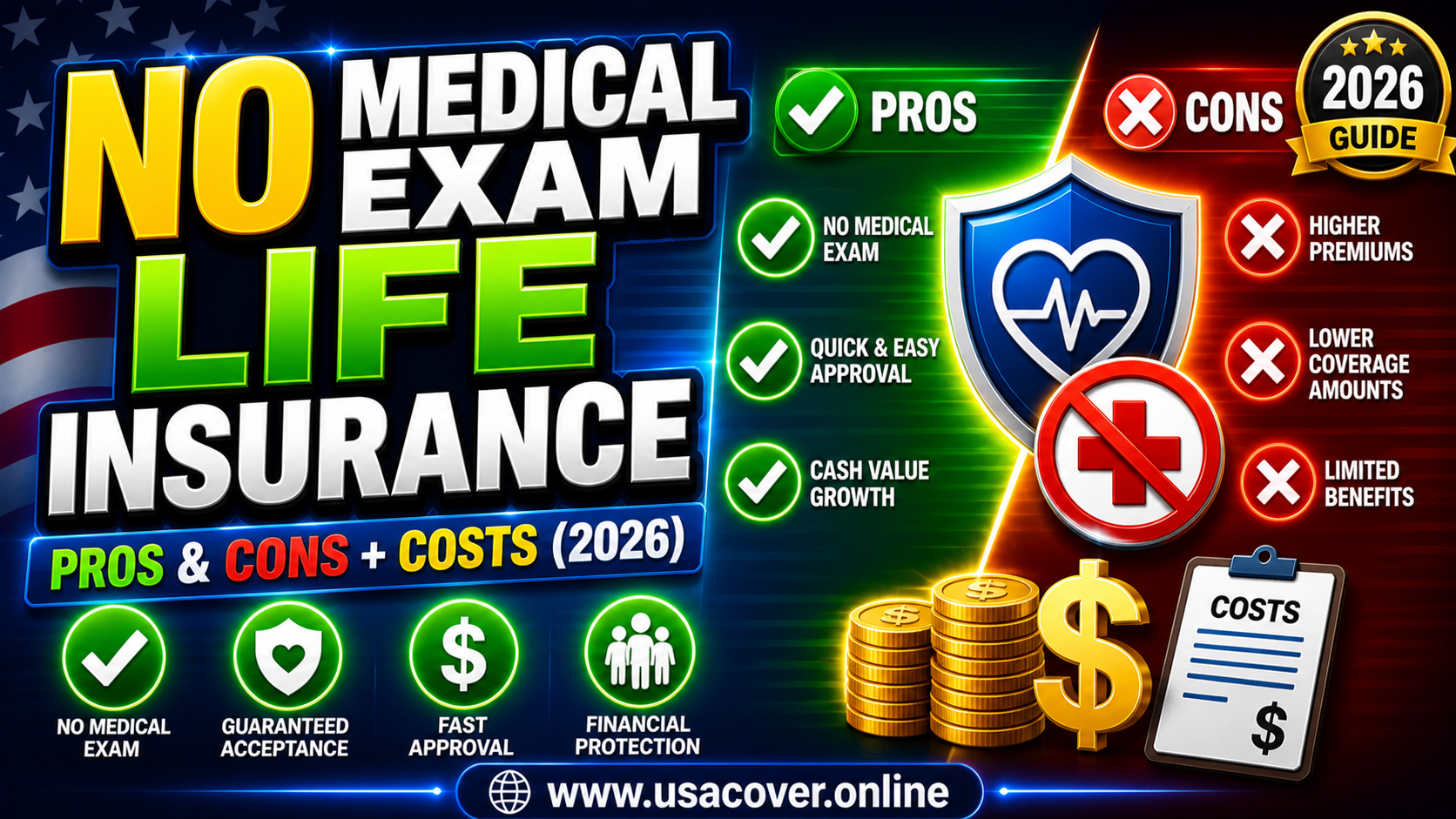

Pros and Cons of No Medical Exam Life Insurance

✅ Advantages

- Fast approval — ideal for urgent coverage needs

- No needles or medical tests

- Accessible for high-risk individuals

- Simple online process

- Useful for seniors or people denied traditional policies

❌ Disadvantages

- Higher premiums (often 20–50% more)

- Lower coverage limits

- Waiting periods (for guaranteed issue)

- More reliance on data accuracy

- Limited policy customization

Quick Comparison Table

| Feature | No Medical Exam | Traditional Life Insurance |

|---|---|---|

| Approval Time | Minutes to days | Weeks |

| Medical Exam | Not required | Required |

| Premium Cost | Higher | Lower |

| Coverage Limit | Moderate | High |

| Eligibility | Easier | Stricter |

Who Should Consider No Exam Life Insurance?

Best Fit Scenarios

This type of policy works well if you:

- Have pre-existing health conditions

- Are over age 50

- Need coverage urgently

- Were denied traditional insurance

- Prefer a fast, hassle-free process

Not Ideal If You:

- Are young and healthy

- Want the lowest possible premiums

- Need large coverage amounts ($500K+)

Real-World Use Cases

Scenario 1: Health Concerns

A 58-year-old with diabetes may struggle with traditional underwriting but can get approved quickly through a no-exam policy.

Scenario 2: Time-Sensitive Coverage

A parent securing a loan may need immediate coverage—no exam policies provide fast solutions.

Scenario 3: Backup Coverage

Some buyers use no-exam policies as temporary protection while applying for a traditional plan.

Cost of No Medical Exam Life Insurance in the USA

Typical Price Range

- $15–$150/month depending on:

- Age

- Health status

- Coverage amount

- Smoking status

(Source: Industry averages, 2024)

Cost Comparison Example

| Profile | Traditional Policy | No Exam Policy |

|---|---|---|

| 30-year-old healthy | Low | Slightly higher |

| 55-year-old smoker | High or declined | Higher but approved |

Why Is It More Expensive?

Insurance companies take on more risk without a medical exam.

To offset this, they:

- Increase premiums

- Limit coverage

- Use conservative underwriting models

Companies like Prudential Financial and AIG use predictive analytics to manage this risk.

Key Decision Framework: Is It Worth It?

Use this quick evaluation:

Step 1: Urgency

- Need coverage now → Choose no exam

- Can wait → Consider traditional

Step 2: Health Status

- High risk → No exam is practical

- Healthy → Compare both options

Step 3: Coverage Needs

- <$250K → No exam works

- $500K → Traditional preferred

Step 4: Budget

- Tight budget → Avoid higher premiums

- Flexible → Convenience may justify cost

Common Mistakes to Avoid

- Choosing guaranteed issue when simplified issue would suffice

- Ignoring waiting periods

- Overpaying without comparing quotes

- Providing inaccurate health information

- Assuming all policies offer instant approval

Alternatives to Consider

1. Fully Underwritten Life Insurance

- Lower premiums

- Higher coverage

- Requires medical exam

2. Employer-Sponsored Group Insurance

- No exam required

- Limited coverage

- Not portable

3. Hybrid Accelerated Policies

- Balance between cost and speed

- Offered by insurers like MetLife

Best Practices for Buying

- Compare at least 3 providers

- Check insurer ratings (e.g., AM Best)

- Choose the right policy type

- Be honest in your application

- Align coverage with financial goals

Key Questions to Ask Before Buying

- How much coverage do I actually need?

- Can I afford the premium long-term?

- Is there a waiting period?

- What happens if I outlive the policy?

- Are there exclusions or limitations?

Frequently Asked Questions (FAQs)

1. Is no medical exam life insurance worth it?

Yes, if you need quick approval or have health risks. Otherwise, traditional policies are usually more cost-effective.

2. How fast can I get approved?

Some policies offer instant approval, while others take 24–72 hours depending on underwriting.

3. What is the maximum coverage available?

Most no-exam policies offer coverage between $25,000 and $500,000.

4. Are premiums higher than traditional life insurance?

Yes, typically 20–50% higher due to increased insurer risk.

5. Can I be denied coverage?

Yes, except for guaranteed issue policies which accept all applicants.

6. Do these policies have waiting periods?

Guaranteed issue policies often include a 2–3 year waiting period before full benefits apply.

7. Is medical information still checked?

Yes, insurers use databases like the Medical Information Bureau and prescription records.

8. Can I switch to a traditional policy later?

Yes, many people start with a no-exam policy and later apply for a fully underwritten plan.

Conclusion

No medical exam life insurance is a powerful option when speed and accessibility matter more than cost. It opens the door for people who might otherwise struggle to get coverage—but it requires careful evaluation.

If you need fast protection, have health concerns, or want a simple process, it can be the right choice. But if you’re healthy and planning long-term, traditional policies often deliver better value.

The smartest approach is to compare both options, understand your priorities, and choose a policy that fits your financial reality—not just your immediate needs.